HONG KONG, Aug. 25, 2016 /PRNewswire/ -- Galaxy Entertainment Group Limited ("GEG" or the "Group") (HKEx stock code: 27) today reported unaudited results for the three and six month periods ended 30 June 2016.

HIGHLIGHTS

GEG: Continues to Drive Mass Business, Profitable Volumes and Control Costs

Galaxy Macau™: Solid Performance Driven by Mass

StarWorld Macau: Continues Transition to Mass

Broadway Macau™: Continues to Drive Visitations to our Cotai Portfolio

Balance Sheet: Remains Well Capitalized, Liquid and Virtually Debt Free

Development Update: Advancing Plans for Cotai Phases 3 & 4 and Hengqin

Dr. Lui Che Woo, Chairman of GEG said:

"GEG today announced solid financial results for the first half of 2016 as the Macau market continued to show gradual signs of stabilization. Galaxy Macau™, with its large mass segment and non-gaming entertainment amenities, is the main contributor to our results. This coupled with StarWorld Macau's ongoing steady transition to a Mass focused operation illustrates the broadening of GEG's footprint and the expansion of its non-gaming offering."

"Despite the continuing global headwinds and challenging times, Group revenues were steady at $25.5 billion in 1H 2016. Our strong focus on operational efficiency and prudent cost control contributed to our Adjusted EBITDA increasing by 13% in the same period. For Q2, Group revenue was up 4% year-on-year to $12.2 billion and Adjusted EBITDA was up 22% year-on-year to $2.3 billion. Our hotels were virtually fully occupied."

"The Macau market continues to show gradual signs of stabilization. Through the publication of its Interim Review of Gaming Liberalization for Games of Fortune Research Report, Five-Year Development Plan and the Tourism Industry Development Master Plan, the Macau Government has reinforced its commitment to economic growth and its support of the gaming and tourism industries."

"GEG supports the objectives in the recently released Government reports and we continue to enhance our non-gaming offerings to help diversify and grow both GEG revenues and the Macau economy. Moving forward to the second half of 2016 and beyond, we will continue our focus on the mass market while maintaining prudent cost control."

"In terms of development pipeline, GEG has the most clearly defined development plans in Macau, which includes the construction of Cotai Phases 3 & 4 and the proposed Hengqin project. The Cotai Phases 3 & 4 will further bolster GEG's non-gaming footprint by allocating substantial floor space to non-gaming amenities, including MICE, entertainment and family facilities. The proposed Hengqin development will allow the Group to develop a low density integrated resort that will complement our high-energy resorts in Cotai."

"Furthermore, drivers of growth viewed as fundamental to the long-term success of Macau -- such as planned and ongoing major transportation infrastructure projects and synergies between the Macau Government's development policies and the Central Government's 13th Five-Year Plan – are unchanged. These factors are likely to promote increased visitor numbers across tourism, leisure and gaming sectors."

"On 29 April 2016, we paid a special dividend of $0.15 per share, reflecting our continued confidence in the long-term outlook for Macau and our commitment of returning capital to shareholders. We are pleased to announce another special dividend of $0.18 per share to be paid on or about 28 October 2016."

"As a final note, I would like to thank the entire GEG team for their diligent efforts in supporting the Group to achieve these solid and credible results."

Market Overview

The market in the 1H 2016 continued to show gradual signs of stabilization despite the continuing challenging conditions and seasonal factors that impacted revenues. These include the slowdowns in the Chinese and the global economies, uncertainty around the UK's Brexit decision on financial markets, the UEFA Euro 2016 football championship and the tightening regulatory environment.

Gross Gaming Revenue ("GGR") decreased by 11% year-on-year to $104.6 billion in 1H 2016. We believe that the market trend towards mass has continued with total mass GGR now exceeding VIP GGR. Total visitor arrivals in 1H grew marginally by 0.1% year-on-year to 14.8 million and the average length of stay of visitors grew by 0.2 day year-on-year to 1.2 days. Importantly, 1H 2016 overnight visitors grew by 8% year-on-year to 7.2 million due to the opening of additional hotel rooms. Overnight visitors typically spend significantly more on high margin non-gaming services.

Group Financial Results

1H 2016

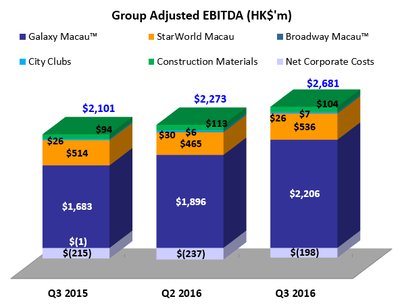

The Group's 1H 2016 results posted revenue of $25.5 billion (1H 2015: $25.4 billion), generating Adjusted EBITDA of $4.7 billion, up 13% year-on-year. As of 30 June 2016, the latest twelve months Adjusted EBITDA was $9.3 billion. Net profit attributable to shareholders was $2.6 billion, including $350 million of non-recurring charges. Galaxy Macau™'s Adjusted EBITDA was $3.9 billion, up 22% year-on-year. StarWorld Macau's Adjusted EBITDA was $977 million, down 12% year-on-year. Broadway Macau™'s Adjusted EBITDA was $9 million.

During 1H 2016, GEG experienced good luck in gaming operations which increased Adjusted EBITDA by approximately $90 million.

The Group's total gaming revenue on a management basis[1] in 1H 2016 was $24.1 billion, down 2% year-on-year as total mass table games revenue was $10 billion, up 22% year-on-year and total VIP revenue was $13.2 billion, down 15% year-on-year.

")

| [1] The primary difference between statutory revenue and management basis revenue is the treatment of City Clubs revenue where fee income is reported on a statutory basis and gaming revenue is reported on a management basis. |

Q2 2016

The Group posted revenue of $12.2 billion, up 4% year-on-year and Adjusted EBITDA of $2.3 billion, up 22% year-on-year in Q2 of 2016. Galaxy Macau™'s Adjusted EBITDA was $1.9 billion, up 34% year-on-year. StarWorld Macau's Adjusted EBITDA was $465 million, down 9% year-on-year. Broadway Macau™'s Adjusted EBITDA was $6 million.

During Q2 of 2016, GEG experienced bad luck in gaming operations which reduced Adjusted EBITDA by approximately $10 million.

The Group's total gaming revenue on a management basis[2] in Q2 of 2016 was $11.5 billion, up 3% year-on-year as total mass table games revenue was $5 billion, up 28% year-on-year and total VIP revenue was $6 billion, down 13% year-on-year.

")

| [2] The primary difference between statutory revenue and management basis revenue is the treatment of City Clubs revenue where fee income is reported on a statutory basis and gaming revenue is reported on a management basis. |

Balance Sheet, Cost Control and Special Dividends

The Group's balance sheet remains healthy. As of 30 June 2016, cash and liquid investments stood at $11.3 billion and net cash was $10.1 billion. Total debt was $1.2 billion as of 30 June 2016 (31 December 2015: $1.2 billion).

Previously we announced an $800 million cost control initiative. Up to the end of Q1 we had delivered $650 million and during Q2 we delivered the remaining $150 million. Importantly, this has been achieved without any local labour redundancies or without compromising our renowned "World Class, Asian Heart" service standard. We have identified an incremental $300 million of additional cost savings which will be delivered in 2016.

The Group paid a special dividend of $0.15 per share on 29 April 2016. Subsequently, the Group will pay another special dividend of $0.18 per share on or about 28 October 2016.

Galaxy Macau™

Galaxy Macau™ is the main contributor to Group revenue and earnings. Galaxy Macau™'s 1H 2016 revenue was $18.5 billion, up 8% year-on-year. Adjusted EBITDA was $3.9 billion, up 22% year-on-year. Q2 Adjusted EBITDA was $1.9 billion, up 34% year-on-year. The Group expects to leverage economies of scale as it continues to see the growth of Macau's mass market. We experienced good luck in our gaming operations which increased Adjusted EBITDA by approximately $155 million in the 1H and $20 million in the Q2.

Adjusted EBITDA margin for 1H 2016 calculated under HKFRS was 21% (1H 2015: 19%), or 27% under US GAAP (1H 2015: 25%). Good luck had a modest impact on margin for 1H 2016.

VIP Gaming Performance

VIP rolling chip volume for 1H 2016 was $245.8 billion, down 16% year-on-year. This translated to revenue of $9.9 billion, down 4% year-on-year. Q2 revenue was $4.4 billion, down 5% year-on-year and 19% quarter-on-quarter.

VIP Gaming

| HK$'m |

Q2 2015 |

Q1 2016 |

Q2 2016 |

QoQ% |

YoY% |

1H 2015 |

1H 2016 |

YoY% |

| Turnover |

137,222 |

130,536 |

115,296 |

-12% |

-16% |

293,867 |

245,832 |

-16% |

| Net Win |

4,659 |

5,458 |

4,408 |

-19% |

-5% |

10,282 |

9,866 |

-4% |

| Win % |

3.4% |

4.2% |

3.8% |

3.5% |

4.0% |

Mass Gaming Performance

Mass gaming revenue for 1H 2016 was $6.5 billion, up 22% year-on-year. Q2 revenue was $3.3 billion, up 30% year-on-year but down 1% quarter-on-quarter.

Mass Gaming

| HK$'m |

Q2 2015 |

Q1 2016 |

Q2 2016 |

QoQ% |

YoY% |

1H 2015 |

1H 2016 |

YoY% |

| Table Drop |

6,542 |

7,734 |

7,834 |

1% |

20% |

12,560 |

15,568 |

24% |

| Net Win |

2,496 |

3,284 |

3,253 |

-1% |

30% |

5,375 |

6,537 |

22% |

| Hold % |

38.2% |

42.5% |

41.5% |

42.8% |

42.0% |

Electronic Gaming Performance

Electronic gaming revenue for 1H 2016 was $828 million, up 19% year-on-year. Q2 revenue was $447 million, up 18% year-on-year and 17% quarter-on-quarter.

Electronic Gaming

| HK$'m |

Q2 2015 |

Q1 2016 |

Q2 2016 |

QoQ% |

YoY% |

1H 2015 |

1H 2016 |

YoY% |

| Slots Handle |

9,579 |

11,542 |

11,661 |

1% |

22% |

17,187 |

23,203 |

35% |

| Net Win |

378 |

381 |

447 |

17% |

18% |

694 |

828 |

19% |

| Hold % |

3.9% |

3.3% |

3.8% |

4.0% |

3.6% |

Non-Gaming Performance

Non-gaming revenue for 1H 2016 was $1.3 billion, up 53% year-on-year. Q2 revenue was $639 million, up 38% year-on-year and down 4% quarter-on-quarter. The combined five hotels registered strong occupancy of 97% for 1H and Q2.

Net Rental Revenue for the Promenade was $357 million for 1H 2016, up 129% year-on-year. Q2 revenue was $161 million, up 61% year-on-year and down 18% quarter-on-quarter.

Non-Gaming

| HK$'m |

Q2 2015 |

Q1 2016 |

Q2 2016 |

QoQ% |

YoY% |

1H 2015 |

1H 2016 |

YoY% |

| Net Rental Rev |

100 |

196 |

161 |

-18% |

61% |

156 |

357 |

129% |

| Hotel Rev / F&B |

364 |

470 |

478 |

2% |

31% |

697 |

948 |

36% |

| Total |

464 |

666 |

639 |

-4% |

38% |

853 |

1,305 |

53% |

StarWorld Macau

StarWorld Macau's 1H 2016 revenue was $5.6 billion, down 22% year-on-year. Adjusted EBITDA was $977 million, down 12% year-on-year. Both declines occurred as Macau faced challenges in the VIP segment. We experienced bad luck in our gaming operations which reduced Adjusted EBITDA by approximately $65 million in 1H 2016 and $30 million in Q2.

Adjusted EBITDA margin in 1H 2016 calculated under HKFRS was 17% (1H 2015: 16%), or 24% under US GAAP (1H 2015: 23%). Bad luck reduced margin by approximately 140 basis points for the 1H 2016.

VIP Gaming Performance

VIP rolling chip volume for 1H 2016 was $105.3 billion, down 34% year-on-year. This translated to revenue of $3.1 billion, down 38% year-on-year. Q2 revenue was $1.5 billion, down 30% year-on-year and down 11% quarter-on-quarter.

VIP Gaming

| HK$'m |

Q2 2015 |

Q1 2016 |

Q2 2016 |

QoQ% |

YoY% |

1H 2015 |

1H 2016 |

YoY% |

| Turnover |

71,448 |

59,200 |

46,090 |

-22% |

-36% |

159,939 |

105,290 |

-34% |

| Net Win |

2,112 |

1,659 |

1,472 |

-11% |

-30% |

5,017 |

3,131 |

-38% |

| Win % |

3.0% |

2.8% |

3.2% |

3.1% |

3.0% |

Mass Gaming Performance

Mass gaming revenue for 1H 2016 was $2.3 billion, up 23% year-on-year. Q2 revenue was $1.1 billion, up 20% year-on-year but down 3% quarter-on-quarter.

Mass Gaming

| HK$'m |

Q2 2015 |

Q1 2016 |

Q2 2016 |

QoQ% |

YoY% |

1H 2015 |

1H 2016 |

YoY% |

| Table Drop |

2,465 |

3,019 |

3,062 |

1% |

24% |

4,795 |

6,081 |

27% |

| Net Win |

951 |

1,178 |

1,141 |

-3% |

20% |

1,890 |

2,319 |

23% |

| Hold % |

38.6% |

39.0% |

37.3% |

39.4% |

38.1% |

Electronic Gaming Performance

Electronic gaming revenue for 1H 2016 was $42 million, down 36% year-on-year. Q2 revenue was $18 million, down 45% year-on-year and down 25% quarter-on-quarter.

Electronic Gaming

| HK$'m |

Q2 2015 |

Q1 2016 |

Q2 2016 |

QoQ% |

YoY% |

1H 2015 |

1H 2016 |

YoY% |

| Slots Handle |

480 |

409 |

386 |

-6% |

-20% |

977 |

795 |

-19% |

| Net Win |

33 |

24 |

18 |

-25% |

-45% |

66 |

42 |

-36% |

| Hold % |

7.0% |

5.9% |

4.7% |

6.8% |

5.3% |

Non-Gaming Performance

Non-gaming revenue in 1H of 2016 was $104 million, down 32% year-on-year. Q2 revenue was $48 million, down 27% year-on-year and down 14% quarter-on-quarter. Hotel room occupancy was 97% for the 1H and Q2.

Non-Gaming

| HK$'m |

Q2 2015 |

Q1 2016 |

Q2 2016 |

QoQ% |

YoY% |

1H 2015 |

1H 2016 |

YoY% |

| Net Rental Rev |

8 |

9 |

9 |

0% |

13% |

16 |

18 |

13% |

| Hotel Rev / F&B |

58 |

47 |

39 |

-17% |

-33% |

138 |

86 |

-38% |

| Total |

66 |

56 |

48 |

-14% |

-27% |

154 |

104 |

-32% |

Broadway Macau™

Broadway Macau™ opened on 27 May 2015. A unique family friendly, street entertainment and food resort, it does not have a VIP gaming component. Revenue for the 1H 2016 was $350 million, while Adjusted EBITDA for the period was $9 million. Revenue for Q2 2016 was $169 million, while Adjusted EBITDA for Q2 was $6 million. We experienced good luck in our gaming operations which increased Adjusted EBITDA by approximately $1 million in 1H 2016 and $2 million in Q2.

Mass Gaming Performance

Mass gaming revenue for 1H 2016 was $246 million. Q2 revenue was $115 million, down 12% quarter-on-quarter.

Mass Gaming

| HK$'m |

Q2 2015 |

Q1 2016 |

Q2 2016 |

QoQ% |

YoY% |

1H 2015 |

1H 2016 |

YoY% |

| Table Drop |

177 |

600 |

503 |

-16% |

184% |

177 |

1,103 |

523% |

| Net Win |

37 |

131 |

115 |

-12% |

211% |

37 |

246 |

565% |

| Hold % |

20.7% |

21.9% |

22.9% |

20.7% |

22.3% |

Electronic Gaming Performance

Electronic gaming revenue for 1H 2016 was $16 million. Q2 revenue was $9 million, up 29% quarter-on-quarter.

Electronic Gaming

| HK$'m |

Q2 2015 |

Q1 2016 |

Q2 2016 |

QoQ% |

YoY% |

1H 2015 |

1H 2016 |

YoY% |

| Slots Handle |

58 |

143 |

137 |

-4% |

136% |

58 |

280 |

383% |

| Net Win |

4 |

7 |

9 |

29% |

125% |

4 |

16 |

300% |

| Hold % |

7.1% |

5.1% |

6.2% |

7.1% |

5.6% |

Non-Gaming Performance

Non-gaming revenue in the 1H 2016 was $88 million and Q2 was $45 million. Hotel room occupancy was virtually 100% for the 1H and Q2 2016.

Non-Gaming

| HK$'m |

Q2 2015 |

Q1 2016 |

Q2 2016 |

QoQ% |

YoY% |

1H 2015 |

1H 2016 |

YoY% |

| Net Rental Rev |

3 |

14 |

14 |

0% |

367% |

3 |

28 |

833% |

| Hotel Rev / F&B |

20 |

29 |

31 |

7% |

55% |

20 |

60 |

200% |

| Total |

23 |

43 |

45 |

5% |

96% |

23 |

88 |

283% |

City Clubs and Construction Materials Division

City Clubs contributed $56 million of Adjusted EBITDA to the Group's earnings for 1H 2016, flat year-on-year. Q2 Adjusted EBITDA was $30 million, up 20% year-on-year. The Construction Materials Division posted Adjusted EBITDA of $205 million in 1H 2016, up 42% year-on-year. Q2 Adjusted EBITDA was $113 million, up 18% year-on-year.

Largest Contiguous Landbank in Cotai, Hengqin and International Development Update

Cotai Phases 3 & 4

With the largest contiguous landbank in Cotai, GEG is uniquely positioned for the medium and longer-term growth in tourism and leisure throughout Asia in general and Mainland China specifically. Cotai Phases 3 & 4 will provide GEG with the opportunity to expand its non-gaming footprint even further. We continue to move forward with our planning of Phase 3 with the potential to commence site preparation works in late 2016 and Phase 4 in 2017, with substantial floor area allocated to non-gaming and primarily targeting MICE, entertainment and family facilities. We expect to be able to provide additional information on our development plans in late 2016 or early 2017.

Hengqin

GEG's concept plan for our Hengqin project continued to progress. Hengqin will allow GEG to develop a low rise, low-density integrated resort that will complement our high energy resorts in Cotai. We anticipate to be able to provide further details later in the year.

International

GEG is continuously exploring opportunities in the overseas markets.

Selected Major Awards in 1H 2016

| Award |

Presenter |

| GEG |

|

| Gaming and Lodging - Most Honored Company |

Institutional Investor Magazine - 2016 All-Asia Executive Team

|

| Best Investor Relations Program - First Place - Nominated by the Buy Side |

|

| Best Analyst Days - First Place |

|

| "The most generous Chinese of Hurun Non-Mainland Chinese Philanthropy List 2016" |

Hurun Report |

| Socially Responsible Operator |

International Gaming Awards |

| Galaxy MacauTM |

|

| Best Integrated Resort |

Asia Gaming Awards |

| Macau Elite Service Award 2015 - The Best Integrated Resort and Hotel Service and Brand |

Exmoo |

| The Most Popular Hotel in Macau - Galaxy Hotel |

Top Magazine - 2016 Quality Life Awards |

| 2015-2018 Macao Green Hotel Award |

Macao Environmental Protection Bureau (DSPA) |

| StarWorld Macau |

|

| TOP 10 Glamorous Hotels of China |

China Hotel Starlight Awards |

| Smiling Enterprise Award - StarWorld Hotel |

Smiling Enterprise Award |

| The Supreme Award for the Most Glamorous Hotel of Asia |

Golden Horse Award of China Hotel |

| Broadway MacauTM |

|

| The Supreme Award for the Most Local Experience Resort in Asia |

Golden Horse Award of China Hotel |

| Construction Materials Division |

|

| 22nd Considerate Contractors Site Award Scheme - Outstanding Environmental Management & Performances - Public Works - New Works - Bronze Award |

Development Bureau / Construction Industry Council |

| BOCHK Corporate Environmental Leadership Awards 2015 - 5 Years+ EcoPioneer Companies - KWP Quarry Co. Ltd. - EcoChallenger - KWP Quarry Co. Ltd. - EcoChallenger - Doran Construction Products (Shenzhen) - EcoChallenger - Fast Concrete Ltd. - EcoChallenger - K. Wah Materials (Huidong) Limited - EcoChallenger |

Federation of Hong Kong Industries / Bank of China (Hong Kong) |

Outlook

GEG delivered solid results during the first half of 2016, despite some challenging conditions and seasonal factors, including: the slowdown in the Chinese and global economies, uncertainty around the UK's Brexit decision on financial markets, the UEFA Euro 2016 football championship and the tightening regulatory environment. Faced with these headwinds, GEG will continue to enhance operational efficiencies, allocate resources to the highest and best use and focus on ongoing prudent cost controls.

There were gradual signs of market stabilization during the half-year period and these were complemented by the encouraging six month performance of Galaxy Macau™ Phase 2 and Broadway Macau™. Their opening in 2015 has provided GEG with a broader mass market offering, significantly expanded the Group's footprint and non-gaming offering and further enriched Macau's tourism offering and enhanced Macau's position as a World Centre of Tourism and Leisure.

GEG sees the market shift towards the mass segment continuing, underpinned by the Government's push towards non-gaming development including MICE, entertainment and family facilities. This market shift will also be supported by improved infrastructure, including the HK-Zhuhai-Macau Bridge, the Taipa Ferry Terminal and the extension of the train line connecting Zhuhai to the Lotus Bridge in Hengqin, a project that will significantly improve access to Cotai. We expect these factors to combine in the short to medium-term to drive increased overnight visitor numbers, whom stay longer, and have a higher non-gaming spend.

With our healthy balance sheet, our capital allocation strategy is to carefully balance returning capital to shareholders through dividends and focusing on our development pipeline to ensure we have the capacity available to capture the future increase in leisure, tourism and travel. This will see the implementation of the Cotai Phases 3 & 4, the largest contiguous landbank of any casino operator in Macau, and the proposed development of the 2.7 sq km Hengqin project.

GEG remains optimistic about the prospects for Macau in general and GEG specifically over the medium to longer-term. GEG believes that the opening of Galaxy Macau™ Phase 2 and Broadway Macau™ helped stabilize the market and slow the rate of decline in overall GGR. While we do acknowledge that there might be increased competition with the opening of additional properties in Cotai, we are hopeful that the new properties will also be a catalyst for increased visitation and increased length of visitor stay. GEG will continue to support the Government in its efforts to create a sustainable and long-lasting gaming industry that not only drives economic development but also ensures Macau's sustainable future.

About Galaxy Entertainment Group (HKEx stock code: 27)

Galaxy Entertainment Group Limited ("GEG" or the "Group") is one of the world's leading hospitality and gaming companies. It primarily develops and operates hotels, gaming and integrated resort facilities in Macau. The Group is listed on the Hong Kong Stock Exchange and is a member of the Hang Seng Index.

GEG is one of six gaming concessionaires in Macau with a track record of delivering innovative, spectacular and industry leading properties, products and services, underpinned by a "World Class, Asian Heart" service philosophy, that has enabled it to consistently outperform the wider market.

GEG operates three flagship venues in Macau: on Cotai, Galaxy Macau™, one of the world's largest integrated destination resorts, and the adjoining Broadway Macau™, a new hotel, entertainment and retail landmark destination; and on the Peninsula, StarWorld Macau, an award winning high end property.

The Group has the largest development pipeline of any concessionaire in Macau. When Phases 3 & 4 of its Cotai landbank are completed, GEG's footprint on Cotai will double to more than 2 million square meters. GEG has also entered into a framework agreement to develop a low rise, low density world class destination resort on a 2.7 square kilometer land parcel on Hengqin adjacent to Macau. This resort will complement GEG's offer in Macau, differentiate it from its peers and support Macau in its vision to become a World Centre of Tourism and Leisure. Additionally, we continue to explore international development opportunities.

GEG is committed to delivering unique 'World Class, Asian Heart' holiday experiences to its guests and building a sustainable future for Macau.

GEG also operates a Construction Materials Division.

For more information about the Group, please visit www.galaxyentertainment.com

Photo - http://photos.prnasia.com/prnh/20160825/8521605377-a

Photo - http://photos.prnasia.com/prnh/20160825/8521605377-b