BEIJING, Aug. 19, 2021 /PRNewswire/ -- The thriving stay-at-home economy that emerged in 2020 unleashed the potential of the cloud-based communications market. Rising alongside the ongoing improvement of the communications infrastructure, the market is entering a golden age. The cloud-based communications market in China will continue to grow rapidly in the coming years and is expected to exceed RMB100 billion by 2024, according to a report from China Investment Corporation (CIC).

With the sector's anticipated growth, industry players are fulfilling expectations by continually delivering notable performances. Recently, Cloopen Group Holding Limited (NYSE: RAAS) ("Cloopen" or the "Company") announced its financial results for the second quarter of 2021. According to the report, the Company's revenues for the second quarter were RMB274 million, representing a 47.9% increase year-over-year or a 33.9% increase quarter-over-quarter. Its core CC (Cloud-based Contact Center) solutions business performed especially well, achieving revenues of RMB108 million, an increase of 105.1% year-over-year. In terms of profitability, the Company's gross margin increased to 43.1%. Adjusted EBITDA loss was RMB29.966 million, while adjusted EBITDA loss margin (as a percentage of revenue) decreased markedly to 10.9%, a nearly 6% decrease year-over-year and an 18% decrease quarter-over-quarter.

Three-month Period Ended, |

|||||||||

June 30, |

June 30, |

June 30, |

|||||||

2020 |

2021 |

2021 |

|||||||

RMB |

RMB |

USD |

|||||||

(in thousands, except for per share data) |

|||||||||

Revenues |

185,255 |

273,905 |

42,422 |

||||||

Cost of revenues |

(113,856) |

(155,805) |

(24,131) |

||||||

Gross profit |

71,399 |

118,100 |

18,291 |

||||||

Operating expenses: |

|||||||||

Research and development expenses |

(36,644) |

(61,970) |

(9,598) |

||||||

Sales and marketing expenses |

(46,643) |

(72,842) |

(11,282) |

||||||

General and administrative expenses |

(46,240) |

(79,664) |

(12,338) |

||||||

Total operating expenses |

(129,527) |

(214,476) |

(33,218) |

||||||

Operating loss |

(58,128) |

(96,376) |

(14,927) |

||||||

Other income (expense): |

|||||||||

Interest expenses |

(4,141) |

(119) |

(18) |

||||||

Interest income |

479 |

1,265 |

196 |

||||||

Loss from disposal of subsidiaries, net |

(335) |

(4) |

(1) |

||||||

Share of income (loss) of equity method investments |

(1,021) |

8 |

1 |

||||||

Change in fair value of warrant liabilities |

722 |

— |

— |

||||||

Impairment loss of long-term investments |

— |

(15,667) |

(2,427) |

||||||

Foreign currency exchange gains (losses), net |

(270) |

4,028 |

624 |

||||||

Loss before income taxes |

(62,694) |

(106,865) |

(16,552) |

||||||

Income tax benefit |

529 |

1,232 |

191 |

||||||

Net loss |

(62,165) |

(105,633) |

(16,361) |

||||||

Cloopen optimized revenue structure by increasing proportion of businesses with higher gross margins

Cloopen, began to provide cloud-based communications solutions in 2014, went public in the US in February of this year, becoming the first Chinese SaaS company to do so. After over a decade of development, the Company's businesses now include communications platform as a service (CPaaS),Cloud-based Contact center (CC) and Cloud-based Unified Communications and Collaboration(UC&C).

In terms of revenue composition, CPaaS revenue reached RMB115 million in the second quarter,maintaining organic growth rate of 13% year-over-year. The high-margin CC and UC businesses contributed more than 50% of total revenue for the first time, and CC solutions contributed significantly to revenue growth. In recent years, the CC solutions market has maintained rapid growth, attracting the attention of the industry's powerful players.

Against the backdrop of a thriving market, Cloopen delivered positive news regarding its CC solutions business. During the reporting period, the Company's CC business achieved revenues of RMB108 million, an increase of over 100% year-over-year.

Two factors account for the exceptional performance of the CC business. First, Cloopen's acquisition of CRM software provider EliteCRM in March of this year and its integration enabled strategic synergies. Second, the Company expanded its CC business by adding CRM and CPaaS products, producing a compound sales effect and further growing market share.

Another part of Cloopen's revenue composition consists of UC&C solutions, which include IM and CV services. Compared to CPaaS and CC solutions, the UC&C solutions business is smaller in volume, having achieved revenues of RMB49 million in the second quarter, an impressive increase of 74.9%.

In addition to strong revenues, Cloopen's performance showed laudable profitability. The financial report revealed the Company's gross margin to be 43.1%, compared to 38.5% in the second quarter of 2020. Cloopen's improved profitability was primarily driven by an increase in the proportion of the Company's higher gross margin businesses. According to previous financial reports, the gross margins of Cloopen's CC and UC&C businesses are considerably higher than that of its CPaaS business. In the second quarter of this year, the proportion of the Company's higher gross margin businesses surpassed 50% for the first time, boosting the overall gross margin while significantly optimizing the Company's revenue structure. Meanwhile, the Company's reduced the red ink considerably, with an adjusted EBITDA loss of RMB29.966 million.

According to Chinese information platform Zhitong Caijing, Cloopen's second quarter financial report showed overall positive results in its core financial data, once again demonstrating indications of growth.

Potential for growth in the industry

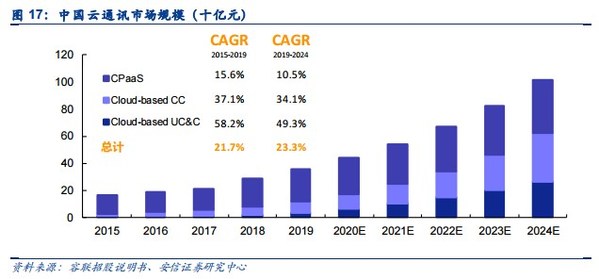

Cloopen is situated within a thriving industry. As aforementioned, the cloud-based communications industry is expected to become a RMB100 billion market in the near future. The CIC report indicated that the cloud-based communication solutions market increased from RMB16.3 billion in 2015 to RMB35.7 billion in 2019, representing a compound annual growth rate of 21.7%.

The market is expected to maintain strong growth momentum. CIC forecasted that the market is expected to reach RMB100 billion by 2024, with a compound annual growth rate of 23.3% during the 2019 to 2024 period.

Cloopen has the potential for greater growth in this market. The cloud-based communications market consists of three major segments: CPaaS, CC and UC&C. Cloopen boasts a comprehensive product portfolio that covers the three major segments CPaaS, CC and UC&C, enabling the Company to accommodate a multitude of business scenarios and provide customers with versatile solutions.

Cloopen also has a competitive edge due to its technology and customer base. First let's consider technological advantages and look at Cloopen's newest product developments as an example. At the World Artificial Intelligence Conference in June 2021 (WAIC 2021), Cloopen debuted Rongxi Robot, which features intelligent voice response systems and outbound solutions, intelligent training capabilities, and AI-assisted customer support. By combining the technologies operating at every level – algorithms at the bottom, AI data in the middle, and AI applications at the top, the Company delivered a comprehensive upgrade of CC solutions that can be applied to the full customer lifecycle.

Next let's examine Cloopen's customer base. According to the financial report, the Company had 12,976 active customers as of the end of June this year, with a dollar-based net customer retention rate of around 110%. A large customer base combined with a high retention rate helps provide the Company's with stable revenues.

Aside from its strong performance, the outlook for the Company's future development is also promising. In terms of its industry, Cloopen conducts business in a fast-growing industry that has entered a golden age. In terms of its performance, there has been continual evidence of the Company's growth. One can expect Cloopen to further unlock its growth potential, owing to its dominant position in product offerings, research and development, and customer base.